Dollar index: Bearish channel keeps short-term buying pressure in check

The dollar upturn eventually lost steam yesterday as there was no significant correction in risk assets following new local high in the S&P 500. The dollar index (DXY) dipped below 104 points:

A bearish correction channel continues to form, as mentioned in the previous article. However, the price is trying to press against the upper bound, as some investors are definitely hoping for a surprise from the Federal Reserve next week. This is also indicated by the technical chart of gold, where the price is pressing against the lower bound of the key channel:

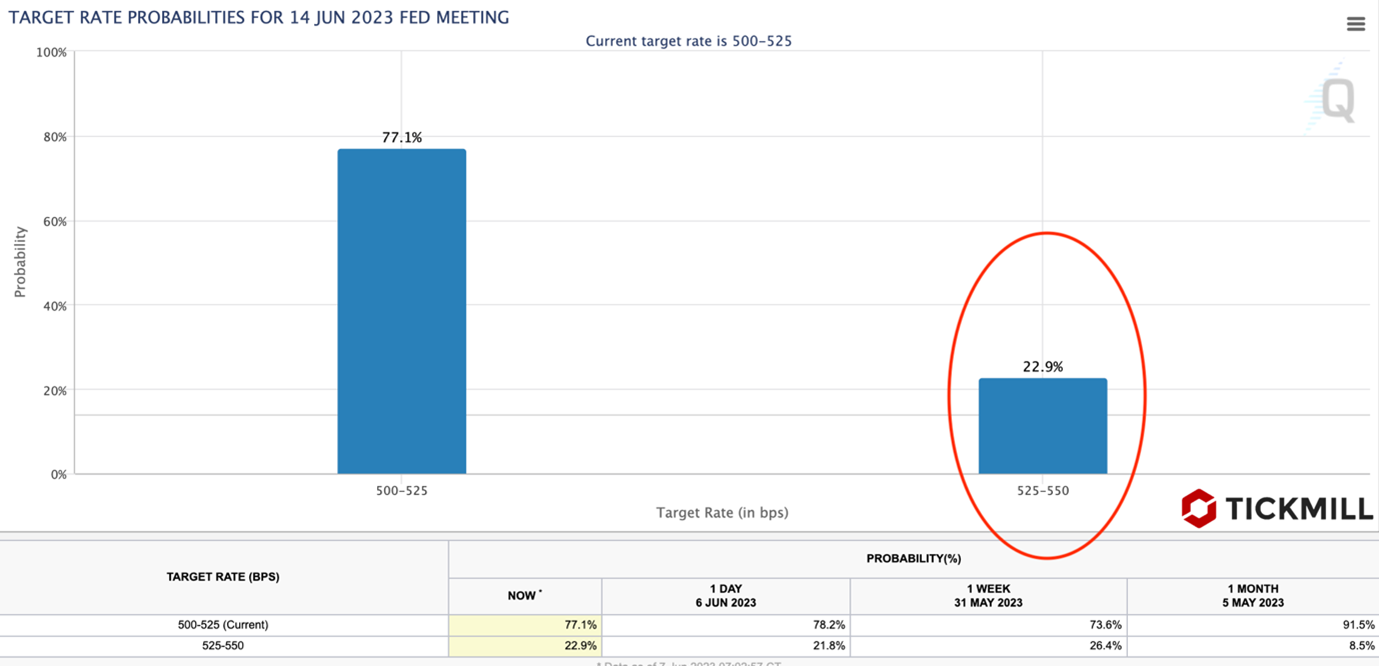

The probability of a rate hike, according to rate futures, is decreasing. This week, the disappointing ISM report on the service sector contributed to this. There is hope that the inflation report for May (scheduled for release on June 13) will once again tilt the scales towards tightening:

Officials from the Federal Reserve (Richard Clarida) and the European Central Bank (Klaas Knot), who spoke yesterday, confirmed their intentions to tighten policy. Knot allowed for two more rate hikes in June and July, after which the course of policy will be determined by incoming data. Clarida stated that the tightening cycle is likely not over and that the rate is unlikely to be lowered before the beginning of 2024.

The Bank of Canada is expected to leave its policy unchanged today, but if there is a rate hike, it will be the second central bank, following the Reserve Bank of Australia, that is not hesitating to tighten. Considering the economic proximity between Canada and the United States, the market may interpret this event as a signal that the Federal Reserve will not lag behind, leading to dollar purchases.

Отказ от ответственности: предоставленные материалы предназначены только для информационных целей и не должны рассматриваться как рекомендации по инвестициям. Точка зрения, информация или мнения, выраженные в тексте, принадлежат исключительно автору, а не работодателю автора, организации, комитету или другой группе, физическому лицу или компании.

Прошлые результаты не являются показателем будущих результатов.

Предупреждение о рисках: CFD-контракты – сложные инструменты, сопряженные с высокой степенью риска быстрой потери денег ввиду использования кредитного плеча. 69% и 73% розничных инвесторов теряют деньги на торговле CFD в рамках сотрудничества с Tickmill UK Ltd и Tickmill Europe Ltd соответственно. Вы должны оценить то, действительно ли Вы понимаете, как работают CFD-контракты, и сможете ли Вы взять на себя высокий риск потери своих денег.

Фьючерсы и опционы: торговля фьючерсами и опционами с маржей несет высокую степень риска и может привести к убыткам, превышающим ваши первоначальные инвестиции. Эти продукты подходят не для всех инвесторов. Убедитесь, что вы полностью понимаете риски и принимаете соответствующие меры для управления своими рисками.