Mixed Economic Signals Across Asia and Global Markets

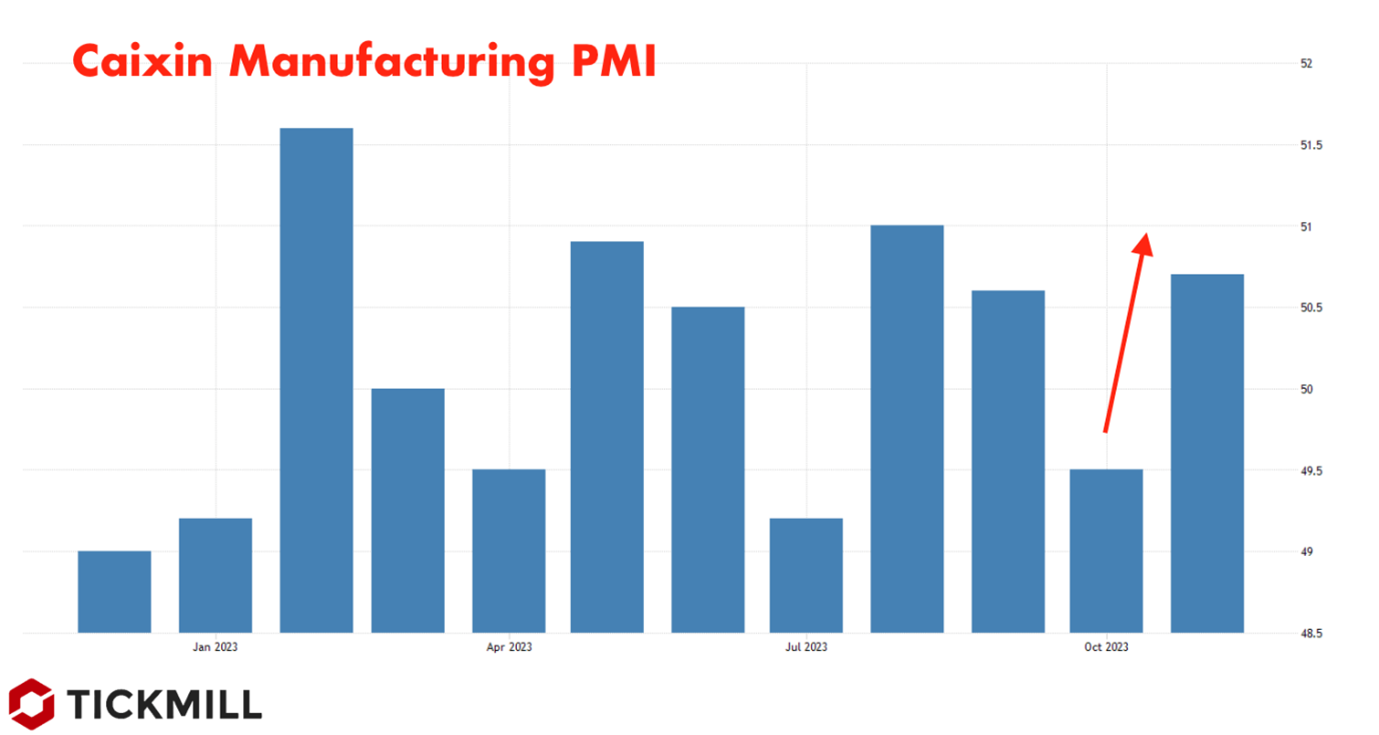

PMI data released on Friday showed that manufacturing activity across Asian countries experienced uneven changes in November. While Japan and Korea saw a slowdown, unexpectedly, private enterprises in China reported improved sentiments compared to the previous month. The relevant index from Caixin Agency rose from 49.5 to 50.7 in November, surpassing expectations that it would change only slightly to 49.8. A reading above 50 indicates a growth in overall sector activity compared to the previous month, in this case, October:

The growth in manufacturing activity in Asia serves as an indicator of increased export activity in these countries. However, a rise in exports also implies an increase in imports, primarily in advanced economies. Essentially, if Asian manufacturing PMI data shows an expansion, it also suggests that global demand remains resilient and that importing firms expect that consumer spending strength will persist.

When considering all key Asian countries, the data for November is mixed. For instance, Vietnam, Malaysia, Taiwan, and Japan had PMI indicators below 50 points in November, while Korea maintained a level of 50 points. In India, the Philippines, Indonesia, and China, the indicators were above 50 points. The overall impression of how the demand in advanced countries importing goods from Asia has changed could be characterized as mildly negative.

The oil market expressed disappointment yesterday with the details of the new OPEC agreement on production caps. The market had priced in an expansion of restrictions by up to 2 million barrels additionally; however, the new cuts amounted to only 900,000 barrels. Brent and WTI prices fell by 3-4 dollars yesterday, and attempts to recover were unsuccessful. Brent is consolidating around $80.5 per barrel, while WTI hovers around $75.50.

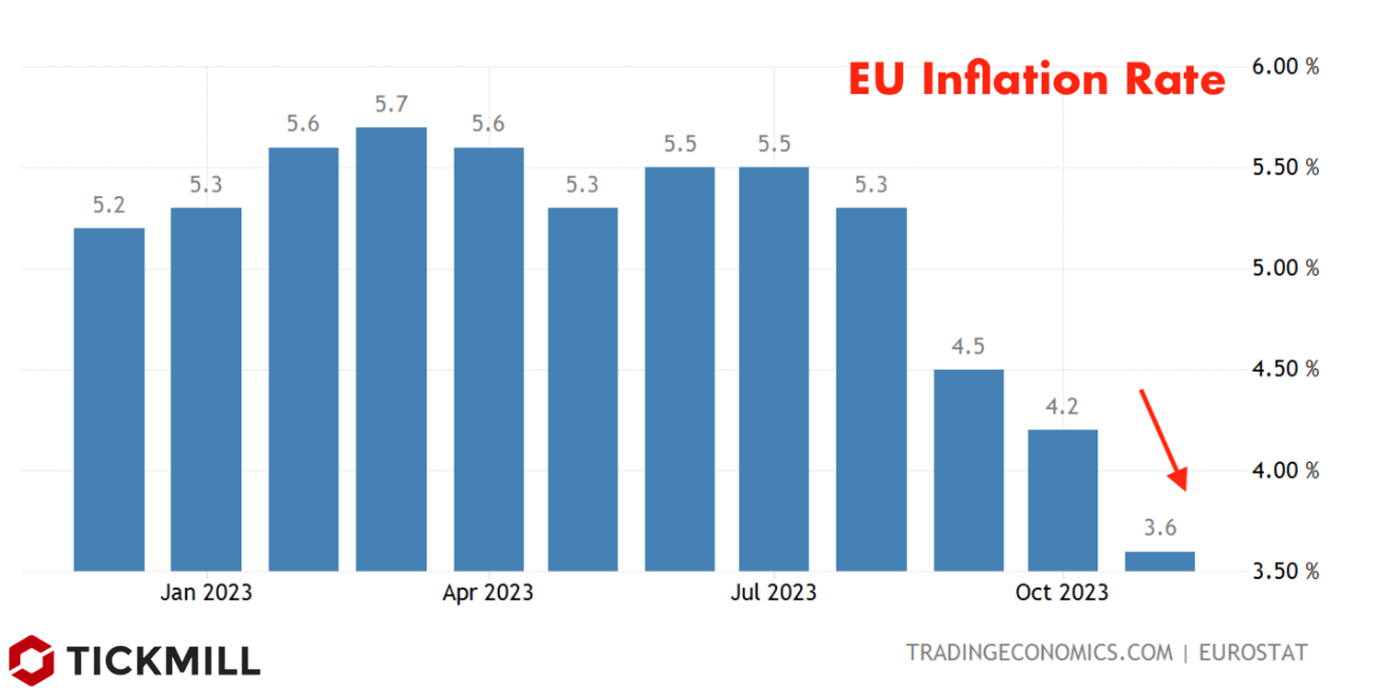

The decline in oil prices did not contribute to the strengthening of currencies for countries importing energy resources. On the contrary, the market was preoccupied yesterday with digesting price data from the EU, which unexpectedly indicated a sharp slowdown in inflation in November. Core inflation in the EU dropped from 4.2% to 3.6%, with the market expecting 3.9%:

This change prompted a reassessment of the timing of the ECB's rate cut and likely forced markets to completely price out a rate hike on upcoming ECB meeting. The balance of expectations regarding the dynamics of rates has shifted in favor of the Fed being perceived as even more hawkish than the ECB. This triggered a correction not only in the Euro but also in the British Pound, as Britain has close economic ties with the EU, and it is expected that the easing of price pressure will spill over, if it hasn't already.

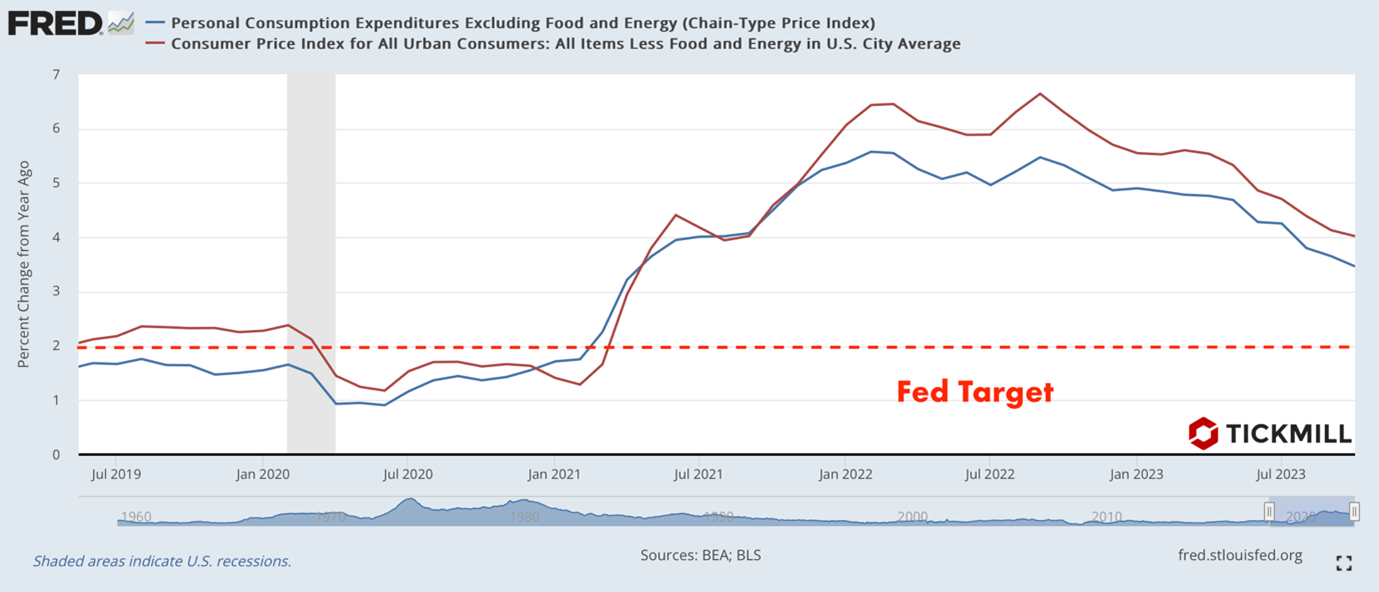

Yesterday also saw the release of the Core PCE indicator for the US. It measures consumer inflation through the pace of growth in consumer spending on a basket of goods and services. The data, for October, arrived after the CPI, but any surprises could have altered market expectations. However, that did not happen; core inflation, in line with expectations, slowed from 3.7% to 3.5%. It's worth noting that the core CPI is also decreasing, and the pace of decline in October exceeded forecasts:

US labor market data additionally facilitated the upward correction of the dollar on Thursday. Initial jobless claims stood at 218,000 (forecasted at 220,000), with the previous figure at 209,000. The trend of accelerating job losses since mid-October is now in question; for the second consecutive week, the data beat forecasts. However, continuing claims are causing concern; in the reporting week, the indicator saw a sharp upward change to 1.927 million against the forecast of 1.872 million.

Federal Reserve representative Williams' remarks on Thursday were ambiguous, much like comments from other Fed officials this week. He suggested both an increase and a decrease in rates, depending on the data. Powell is scheduled to speak today, and as expected, his comments will likely align with the overall tone of other Fed representatives' statements this week.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.