Investment Bank Outlook 13-09-2022

BNY Mellon

Household Debt Drags G10 Commodity FX

One of the most stable groups of positive holdings in iFlow this year has been the G10 commodity currency trio of CAD, NOK and AUD. From initial fears of global stagflation to more recent support from interest-rate hikes, those currencies have understandably been held on an absolute or relative-value basis as a defensive position against the supply headwinds facing other assets. However, momentum in flows has begun to wane.

Positioning undoubtedly is playing a role, especially if on a marginal basis softer global growth will reduce marginal gains for commodities and its derivative asset classes. More importantly, in our view, is domestic factors coming to the fore. After several years of increases in real estate prices arising from demographic demand, as well as low real rates encouraging household leverage, the process is starting to reverse. Beside the obvious implications for FX positioning, how these currencies fare over coming quarters will hold many lessons for non-commodity economies in developed and emerging economies alike where housing and household leverage are similarly moving up the agenda.

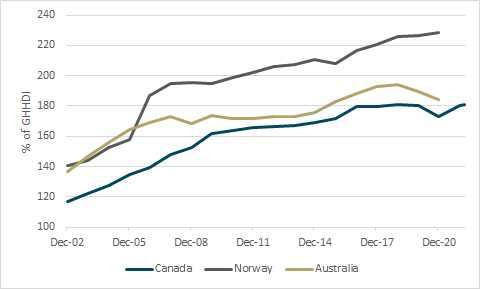

The chart below illustrates household debt-to-income ratios for Canada, Norway and Australia over the past two decades. The most striking aspect of the evolution of leverage is that there was no adjustment during the Global Financial Crisis. For comparison, the US and UK equivalents have declined by 35ppt and 25ppt, respectively, since the 2007 peak; the US is now barely above 100%, which would arguably not qualify as high household leverage at all, despite relatively robust levels of home ownership. There are many structural reasons behind the gains in these countries, a critical one being supply unable to catch up with demand – especially in regions with high demographic growth and household formation.

Central banks often stress that demographics are out of their control, and don’t feature anyway in their monetary policy horizons which normally don’t exceed three years. However, demographic trends in these nations will likely impact potential growth and estimates of neutral rates. In this context, Australia and Canada should already have a demographic premium due to historical reliance on migration for population growth. Norway’s migration policies differ but there will also be pull effects from the rest of the European Union, whose citizens enjoy freedom of movement in Norway. Simply in a regional context, Norway’s population has increased by almost 15% since 2007; Germany's is only up 2.8%.

Norges Bank recently produced a paper signalling real neutral rates between -0.5% and 0.5%. With an inflation target of 2%, neutral nominal rates should have fallen into the 1.5%-2.5% range. Even if we take 2.0% as the threshold, Norges Bank's base rates have only been above that for five months since the end of the GFC. Canada’s record is even starker: a base rate below 2% in the entire post-crisis environment until recently.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

With 10 years of experience as a private trader and professional market analyst under his belt, James has carved out an impressive industry reputation. Able to both dissect and explain the key fundamental developments in the market, he communicates their importance and relevance in a succinct and straight forward manner.