Daily Market Outlook, September 28th, 2021

.png)

Daily Market Outlook, September 28th, 2021

Overnight Headlines

- Australian Household Spending Drops For Third Month On Lockdowns

- China’s Industrial Firms Profit Growth Slowed Further In August

- Japan EconMin: Gov Seeks To Lift State Of Emergency On October 1st

- Some In BoJ Warned Japan's Recovery Might Be Delayed - July Mins

- Australian Treasurer Frydenberg Signals Home Loan Curbs - AFR

- New Zealand Releases Draft Law Aimed At Cooling Housing Market

- China Power Shortage To Ease Amid Steps To Ensure Supply: Daily

- Japan: N.Korea May Have Launched Ballistic Missile - Kyodo

- World Bank: Delta Variant Slowing Economic Growth In East Asia And Pacific

- Fed's Powell: Reopening Economic Bottlenecks Could Be "More Enduring"

- Fed’s Brainard: Labour Market, Inflation Can Return To Pre-Pandemic

- Fed’s Williams: Tapering Bond Buying ‘May Soon Be Warranted’

- Fed’s Evans: US Economy ‘Close’ To Meeting Bond Taper Threshold

- Kaplan Steps Down As Dallas Fed Chief, Hours After Rosengren

- U.K. Opposition Gears Up for Johnson to Call Election Next Year

- Japanese Yen Weakens To 111 Per Dollar As U.S. Treasury Yields Soar

- US Treasuries Face Risk of Prolonged Selloff From Convexity Hedging

- US Sec Gensler: Crypto Markets Will ‘Not End Well’ Without Regulation

- Brent Oil Hits $80 A Barrel For The First Time Since Oct. 2018

- Asia Markets Grapple With Evergrande Fallout. Eye China Power Crunch

- Ford, Korea's SK Invest $11.4b On U.S. Battery, EV Truck Plants

- BHP Shareholders Advised To Vote Against Climate Plan Next Month

- US Bank Stocks Surge Toward Best Year Since 1997 On Fed Shift

The Day Ahead

- Asian equities are mixed this morning with Chinese indices up but other markets mostly down. The US Senate voted down a bill yesterday that would have averted a government shutdown and potential problems with the debt ceiling in October. In Germany, the centre left SPD party has declared its intention to form a coalition government with the Greens and the liberal FDP. Reports suggest that the Army has been put on standby to help ease supply issues at UK petrol stations after a fourth day of queues and pump closures. The latest reading for German consumer confidence unexpectedly rose with the index moving into positive territory for the first time since April 2020.

- The rest of today’s data calendar is very light with nothing of note in the UK or the Eurozone. In the US, the Conference Board’s consumer confidence indicator may get more than usual attention given recent mixed signals on the outlook for the US consumer. In August both this measure and an alternative indicator on consumer sentiment from the University of Michigan fell sharply. That may reflect concerns about both the increase in Covid cases over the summer months and this year’s sharp rise in inflation. A stronger than expected August outturn for retail sales will have provided some reassurance that consumer spending is holding up for now. However, given that the Univ of Mich measure posted only a marginal rebound in September it will be interesting to see whether today’s data provides any better news. Also out in the US are August data for international trade in goods.

- US Federal Reserve Chair Powell and Treasury Secretary Yellen are scheduled to speak before a Congressional Committee today. Their testimony is supposed to be about the effectiveness of measures undertaken to support the economy during the pandemic but other issues are also likely to be covered. Already released written testimony from Powell said that with supply bottlenecks lasting longer than anticipated inflation is set to remain high in coming months before moving back to the 2% target later in 2022. During the question period Powell seems certain to be asked about last week’s news that the Fed will soon start to taper its asset purchases. Meanwhile, with a partial government shutdown in the offering if a Federal budget is not passed by Friday, fiscal policy seems bound to be a focus.

- In a busy week for public appearances by central bankers a number of others are scheduled to speak today. These include Catherine Mann who is a new member of the Bank of England’s Monetary Policy Committee.

G10 FX Options Expiries for 10AM New York Cut

(Hedging effect can often draw spot toward strikes pre expiry if nearby)

- USDJPY - 110.90/111.00 941m. 110.40/50 1.56bn (1.28bn C). 110.00/10 1.16bn (598m C). 109.60/70 643m.

- EURUSD - 1.1950/60 924m. 1.1850/60 614m. 1.1830/40 558m. 1.1790/1.1800 1.72bn (1.15bn C). 1.1770/80 822m. 1.1750/60 1.17bn (693m C). 1.1720/30 637m. 1.1700 529m. 1.1670 423m.

- AUDUSD - 0.7260/70 747m. 0.7250 1.46bn (873m P). 0.7230/40 669m.

- USDCAD - 1.2900 630m. 1.2820/30 990m. 1.2800/10 1.64bn (1.37bn C). 1.2670 3.03bn (2.51bn P). 1.2650 648m. 1.2600/10 1.77bn (1.18bn P).

- EURGBP - 0.8470 420m.

- USDCHF - 0.9130 580m.

- EURCHF - 1.1050 416m. 1.0950 402m.

- AUDJPY - 80.50 490m.

- USDTRY - 8.25 482m.

- USDZAR - 15.50 497m. 14.50 450m.

- USDMXN - 19.45 402m.

- USDCNH - 6.57 730m. 6.54 597m. 6.50 482m. 6.49 527m. 6.46 870m. 6.45 1.70bn (1.22bn P)

Technical & Trade Views

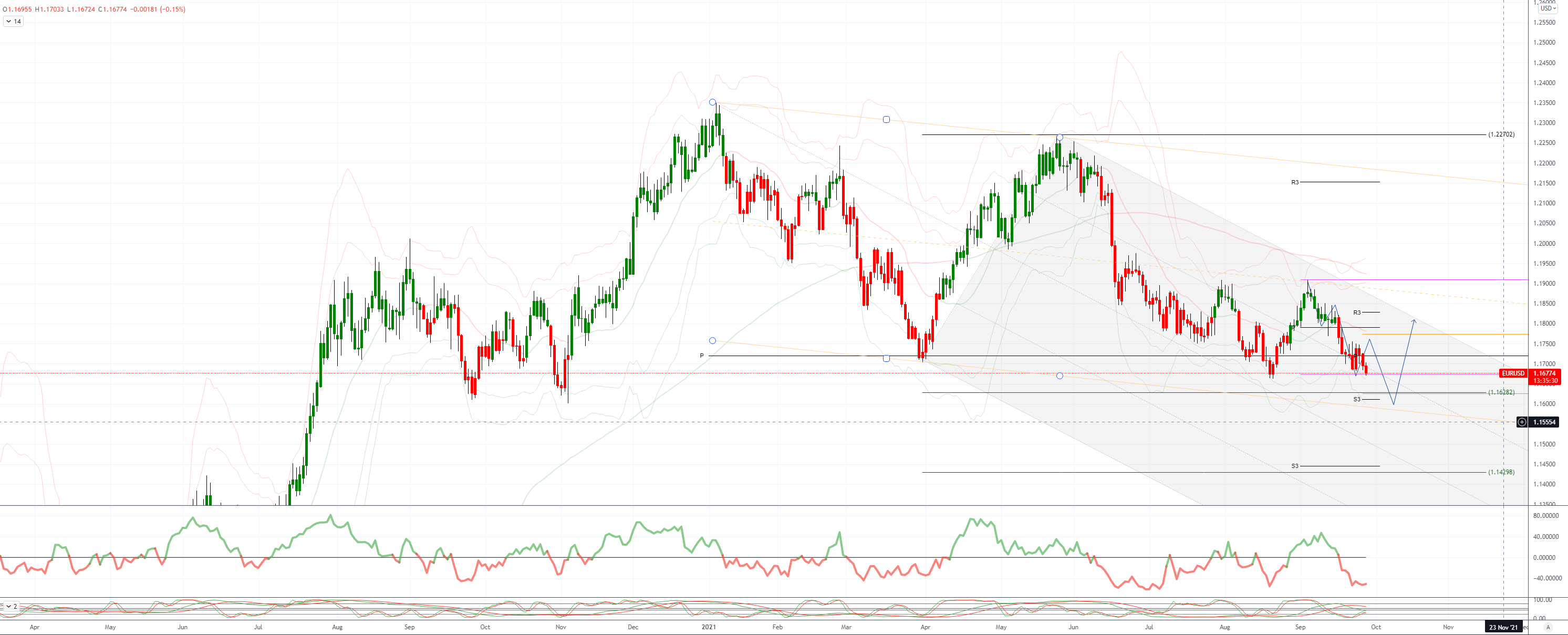

EURUSD Bias: Bearish below 1.19 Bullish above

- EUR/USD sinks towards August low as traders turn to dollar

- EUR/USD sinks 1.1674 EBS triggering tops under lows seen after Fed meeting

- Aug 20 low at 1.1664 and likely more stops below at risk

- Oddly vols remain extremely low with one-month EUR/USD just 4.5

- Vols should rise or EUR/USD reverse, current situation unlikely to last

- Major supports are not too far off now, 100/200-WMAs 1.0602/1.1574

- Weekly Ichimoku cloud base is 1.1538. Major Sep/Nov 2020 lows 1.1613/02

- Seems traders seek safety in USD as well as factoring Fed taper

GBPUSD Bias: Bearish below 1.39 Bullish above.

- Resilient as UST yields climb, slew of BoE speeches

- Steady at the top of a 1.3689-1.3705 range, occasional flurries of interest

- No tier 1 UK data, but BoE's Bailey and 3 other BoE officials to speak

- Unlikely to contradict Monday's hawkish Governor Bailey's stance

- Resilient after early dip below 1.3700 proved short lived - EUR/GBP -0.1%

- UST yields firmer after US debt ceiling failure - 2yr +3bp to 0.313%

- Charts; momentum studies, 5, 10 & 21 DMAs conflict - mixed signals

- 21 day Bollinger bands expand - bias still lower while 1.3763 21 DMA caps

- Double bottom support above 1.3600 vulnerable, as 1.3710 10 DMA holds

USDJPY Bias: Bullish above 109 Bearish below

- USD/JPY on way towards 111.66 test? CB – yields in play

- USD/JPY, JPY crosses on up-up on CB expectations, higher yields abroad

- USD/JPY 110.94 to 111.24 EBS, stops 111.20+ taken out, on way to 111.66?

- Move higher despite continued sales from Japanese exporters - not so large

- 111.66 high of year on July 2, double top July 1-2 111.64-66

- Hawkish Fed expectations, higher US yields behind move, Tsy 10s @1.509%

- BoJ, SNB likely last of major economy CBs to end stimulus...

- JPY crosses bid too, some more than others, GBP/JPY and CAD/JPY shine

- GBP/JPY 151.89 to 152.45, CAD/JPY 87.77 to 88.26...

- EUR/JPY 129.70 to 130.06 EBS, AUD/JPY 80.61 to 81.26

AUDUSD Bias: Bearish below 0.75 Bullish above

- Dalian iron ore falling close to 5%

- AUD/JPY buying flows pushing cross higher and underpinning AUD/USD

- Resistance is at daily highs at 0.7315/20 with sellers ahead of that level

- More resistance comes in at 0.7325/30 where the 21 & 55-day MAs converge

- Support is at 0.7220/25 where multiple daily lows are found

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 71% and 74% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!