Daily Market Outlook, March 21, 2022

Daily Market Outlook, March 21, 2022

Overnight Headlines

- White House: US Pres Biden To Visit Poland On Europe Trip This Week

- China Keeps Benchmark Lending Rates Unchanged, As Expected

- NZIER Forecasts Show A Mixed Growth Outlook Amidst Higher Inflation

- New Zealand Posts Monthly Trade Deficit Of NZ$-385Mln In February

- Hong Kong Eases Travel Curbs That Hit Economy And Sparked An Exodus

- ECB's Holzmann Argues Again For Rate Rise - Austrian Paper

- ECB's De Guindos: ECB Would React To Second-Round Inflation Effects

- ECB's Knot: Interest Rate Increase Later This Year Is Realistic Outlook

- Oil Climbs As Traders Gauge War In Ukraine, Middle East Tensions

- Asia Share Markets Start The Week In A Cautious Mood, Yen Near 6 Year Lows

- China Newspapers See A-Share Opportunities Over Policy Support - CSJ

- Shanghai Disney Closed Until Further Notice As China Battles COVID

The Day Ahead

- Risk sentiment has started the week on a soft note with most major equity indices across the Asia-Pacific lower on the day. Events in Ukraine continue to be the overarching driver for the major asset classes, with the focus on yet another round of negotiation talks later today, following Russia’s demand that Ukrainian troops leave Mariupol, which was rejected by Ukraine. Later this week, NATO heads of state – including US President Joe Biden – will gather to discuss next steps in relation to the conflict.

- Geopolitics is likely to continue to induce global financial market volatility, as the war in Ukraine enters its fourth week. China appears to be treading a broadly neutral path, but the West is looking to see whether it is assisting Russia financially or militarily.

- From a financial market perspective, the sharp rise in commodity prices triggered by the war in Ukraine continues to present significant policy challenges for central banks.

- Accompanying last week’s decision by the US Federal Reserve to raise interest rates by 0.25%, the so-called ‘dot plot’ projections signalled a median expectation amongst policymakers of six further 0.25% increases (potentially one at each of its remaining FOMC meetings) this year, with three to four more hikes in 2023 to 2.75% - above its estimate of the longer-term neutral rate. That suggests the Fed remains preoccupied by the need to tame inflation. With the ‘dot plot’ capturing the views of both voters and non-voters of the FOMC, a busy slate of speakers this week – including Fed Chair Powell today, will give markets an opportunity to assess how the 2022 voting members are positioned particularly in light of developments in Ukraine. Elsewhere, the lack of any key data means the focus will remain on policymakers. ECB members Makhlouf and Nagel are scheduled to speak at events today.

- Early tomorrow morning, the February UK public finances will provide a timely reminder of the health of the domestic fiscal position ahead of the Chancellor’s Spring Statement on Wednesday. Government borrowing looks on course to have halved to around £160bn in the current financial year, compared with £183bn predicted last October. Moreover, the strong labour market may continue to buoy tax receipts going forward.The latest figures are expected to further highlight this and provide a more accurate assessment of how much the government has over-funded itself in the current fiscal year, which will provide the Chancellor with wiggle room to provide some giveaways, especially to those more affected by the soaring cost of living. Media reports suggest that a limited package of measures is being put together by the Treasury, which could include a fuel duty cut and a raising of the threshold at which people start paying national insurance.

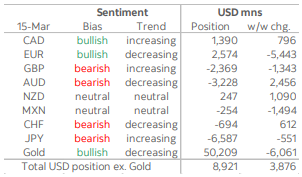

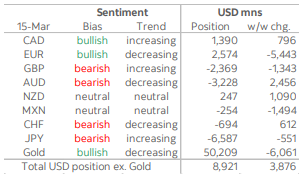

CFTC Data

- After practically no change last week, the overall USD long saw its first increase since midJanuary with IMM positioning data showing a large net USD3.9bn bet in favour of the USD amid mixed adjustments in the currencies that we cover. On Tuesday, the Bloomberg Dollar Index (BBDXY) reached its strongest level since July 2020 ahead of the Fed’s policy announcement on Wednesday and on the back of continued market anxiety over the war in Ukraine.

- EUR sentiment worsened sharply as net EUR longs that were cut by USD1bn last week were reduced further by a massive USD5.4bn, its sharpest one-week-drop since mid-2018. The EUR long fell to a ten-week-low of USD2.6bn. The EUR extended its bounce off the 1.08 zone last week but investors slashed long bets while leaving gross short contracts relatively steady.

- Alongside a 2.2% depreciation that took the yen to its weakest level since late-2016, the large JPY net short climbed by a relatively modest USD551mn, undoing only part of the USD1.4bn adjustment in its favour last week, to sit at USD6.6bn as of Tuesday. A hawkish Fed, a very dovish BoJ, and strong commodity prices pose significant headwinds for the JPY.

- With the GBP hitting a fifteen-month low of 1.30 this week, net GBP shorts rose by USD1.3bn to USD2.6bn, the biggest bearish bet on the pound since early-2022. A dovish hike by the BoE on Thursday highlighted the limited tailwinds for sterling that will likely sustain a bearish GBP position over the coming months.

- The CAD position more than reversed last week’s decline with a USD796mn move in its favour to climb to the USD1.4bn mark amid a steep reduction in shorts combined with unchanged gross longs. Steadying market volatility and ongoing support from high crude oil prices have helped the CAD since the data cutoff date.

- Speculative positioning in the AUD and NZD materially improved this week as investors cut their net shorts by USD2.5bn and USD1.1bn to short USD3.2bn and now long USD247mn, respectively. This still leaves the AUD position as the most bearish among those covered here after the JPY, but investors may be warming up to the AUD after leading all the G10+MXN currencies for the month (outstanding longs are at a three-month high). The NZD short flipped to marginally long as it pulls away from a negative position that neared the USD1bn mark in early -March and represented the most bearish NZD bet in two years.

- Finally, the MXN’s net long was cut to a net short of USD254mn on a USD1.5bn bet against it as a large number of longs got taken out while shorts increased by roughly 2/3 of the decline in longs. This move comes while the peso stages a strong rebound from the ~21.50 pesos per USD zone where it traded last week; its 2.7% gain over the period more than doubled that of the CAD (the next best performing currency covered here). CHF sentiment did a U-turn of the USD768mn move in its favour last week as investors added USD612mn to the now USD694mn CHF net short

G10 FX Options Expiries for 10AM New York Cut

(Hedging effect can often draw spot toward strikes pre expiry if nearby (P) Puts (C) Calls )

- EUR/USD: 1.1100 (2.79BLN), 1.1150 (646M)

- USD/JPY: 117.00-05 (980M), 118.00 (635M)

- 118.95-00 (695M). GBP/USD: 1.3095 (664M)

- USD/CAD: 1.2740-50 (1.4BLN)

- EUR/CHF: 1.0300 (692M)

Technical & Trade Views

EURUSD Bias: Bearish below 1.15 Bullish above

- Consolidates around 1.1050 in listless Asian trading

- EUR/USD traded in a 1.1040/57 range in Asia after closing Friday at 1.1050

- The Tokyo holiday and lack of weekend market moving news made it a long day

- Market shrugged off hawkish comments coming from the ECB

- EUR/USD not trending and looks set for period of range trading

- Support is @ the 10-day MA @ 1.1000 and break would suggest top is in place

- Resistance is at the 21-day MA at 1.1081 and close above eases pressure

- News related to Russia-Ukraine conflict may impact EUR sentiment

GBPUSD Bias: Bearish below 1.36 Bullish above.

- Soft in a low key session, all eyes on Ukraine

- -0.15% at the base of a quiet 1.3158-1.3171 range - USD a touch firmer

- Ukraine led caution - E-mini S&P -0.25%, Brent +2.6% AsiaxJP stocks -0.1%

- Euroclear joins bank-backed blockchain payment system

- Move is a step towards the next era of faster, cheaper global settlement

- Charts; momentum studies rise - 5, 10 & 21 daily moving averages conflict

- 21 day Bollinger bands contract - mixed signals favour range trading

- Last week's sustained 1.3109 10 DMA break suggests a period of consolidation

- 1.3001 March 2022 low and 1.3246, 38.2% Feb-Mar fall viable range parameters

USDJPY Bias: Bullish above 114.50 Bearish below

- Steady, capped by Ukraine led cooling risk appetite

- Flat at the base of a 119.14-119.30 range as risk soured - Tokyo holiday

- Ukraine conflict continues to escalate, peace talks impasse

- E-mini S&P -0.25%, Brent oil +2.6%, AsiaxJP -1.1% - modest risk off

- Charts - 10 days of higher daily high's sustains the topside bias

- Targets a break of major long term 119.52 resistance 76.4% 2015-2016 fall

- Close above 119.60 opens door to psychological 120.00 then 121.70 2016 peak

- Close below rising 117.47 Tenkan line needed to undermine topside bias

- NY 119.08-119.40 range on Friday is initial support and resistance

AUDUSD Bias: Bullish above .7100 Bearish below

- AUD/USD opened 0.7415 after rising 0.54% in Friday's risk on trading

- After dipping to 0.7405 it moved above Friday's high to trade at 0.7424

- Move up was helped by steady equities and rising commodities

- The mood tempered a bit and E-minis went negative after opening +0.30%

- AUD/USD drifted lower and is at the session low around 0.7400

- Resistance is at the March 7 high at 0.7440

- Supprot comes in at the 10-day MA at 0.7312

- AUD/USD trending higher with the 5, 10 and 21-day MAs in a bullish alignment

- Only a break below the 10-day MA would suggest trend is waning

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!